Flow Traders: Into the Too Hard Basket

Rubbing My Nose In It

"I know I'll perform better if I rub my nose in my mistakes. This is a wonderful trick to learn."

Charlie Munger

Executive Summary

My initial understanding of Flow Traders and its industry of market-making has turned out to be less thorough than I believed. Data recently brought to my attention has revealed that Flow Traders is losing market share in Europe, where I thought it held a strong competitive edge. This has made me realise that my grasp of the company’s business model and market dynamics wasn't as solid as I initially thought. Given these uncertainties and the company's underperformance, I've decided to label Flow Traders as 'too hard' to evaluate and exit my position.

Initial Thesis

You can read my original article here: My Initial Article.

In my initial analysis of Flow Traders, I viewed it as a form of portfolio "insurance". The idea was that Flow Traders would perform moderately well in normal market environments, distributing regular dividends, but would significantly outperform during market downturns. This outperformance, driven by increased market volatility, would lead to higher dividends and a rising stock price, providing additional capital precisely when other stocks are cheaper to buy.

Flow Traders exemplified this behaviour during the 2020 market crash induced by COVID-19. As the VIX, a key measure of volatility, soared to 65.5—its highest level since 2008—Flow Traders saw its revenues nearly triple, with profits rising nearly nine fold compared to the prior year. The company's dividend payout also surged, tripling year-over-year.

Prior to Covid19, since its IPO in 2015, Flow Traders had consistently delivered growing Earnings Per Share (EPS) and dividends, making it an attractive income-generating asset. The core idea behind my investment was that this consistent dividend growth would be supplemented by outsized gains during volatile market periods, giving investors extra liquidity at the perfect time to invest in falling stock prices.

What Went Wrong with My Flow Traders Investment Thesis

Since I started following and investing in Flow Traders, about a year before writing my initial article, their financial results have consistently worsened. So although it had outperformed over Covid it was not performing that well outside of times of market volatility as I had expected.

At the time, I attributed this decline to lower market volatility, reasoning that narrower bid-ask spreads—where Flow Traders earn their profits—reduced their income opportunities. However, I later realised that although there has been lower volatility there has also been high growth in their trading markets.

Flow Traders highlights in its investor relations materials the growth of the Exchange-Traded Products (ETP) markets, which should have provided more trading opportunities. While narrower bid-ask spreads can decrease profit per transaction, the expanding ETP market should have led to a higher volume of transactions. In fact, the ETP market has been growing at an impressive 20% annually, as shown in the graphic below from Flow Traders investor relations material.

Analysis of long standing data recently brought to my attention has revealed a concerning trend in Flow Traders key European operations. By examining the "Market ETP Value Traded" and "Flow Traders ETP Value Traded" data, I have calculated the Flow Traders' market share in Europe since 2016. Contrary to my belief that Flow Traders held a strong competitive advantage in this region, their market share has steadily declined from approximately 50% in Q4 2016 to just 25% by Q4 2024. This wasn’t a sudden anomaly but a clear downward trend over time.

Beyond market share, it is difficult to assess how well Flow Traders is performing relative to competitors. Flow Traders operates in a niche where the majority of their income is generated without direct customers. With only one significant publicly traded competitor—Virtu Financial—it’s challenging to get a comprehensive view of how Flow Traders' systems and business model stack up.

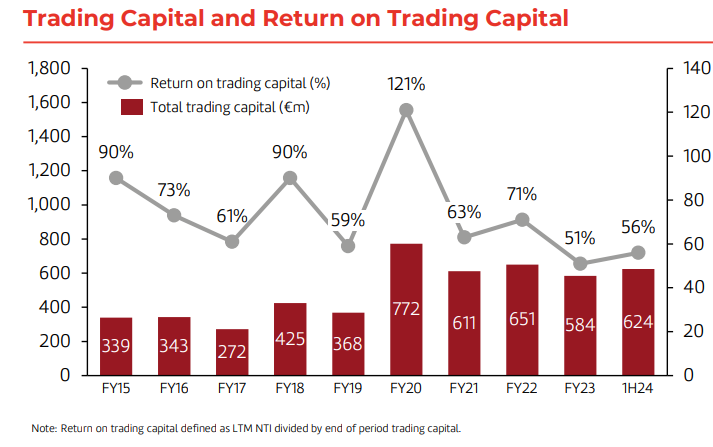

Additionally, another worrying sign was the sharp decline in their return on traded capital, which had been consistently high but has significantly fallen since 2020, further signaling reduced profitability.

They have recently stopped paying a dividend and even have plans to borrow money so that they have more trading capital. Some investors have praised this move, suggesting that the capital previously used for dividends could now generate returns of 50% or more as trading capital like in the chart above. However, this same argument was made when the dividend was cut the first time, and if this is the case it raises questions about Flow Traders’ capital allocation abilities. If they could achieve such high returns by reinvesting the money, why were they paying dividends all along instead of maximising those potential gains for their investors with 50%+ returns?

The main way I would interpret their falling financial results and loss of market share in their key market is declining competitiveness. There may be other reasons but I am not knowledgeable enough about the industry to really know and so that is the only conclusion I can make and why I have decided to put this stock in the too hard pile.

Lessons Learnt

The Risk of Investing in Complex and Opaque Industries

A solid understanding of the industry a company operates in is essential for making sound investment decisions. When dealing with companies in highly complex and opaque industries, caution is necessary. Such investments should either be avoided or approached with a significant margin of safety due to the inherent uncertainties.

High-Frequency Trading (HFT) is one such industry. It involves using powerful computers and advanced algorithms to analyse massive amounts of market data, executing lots of trades at high speeds to exploit short-term market inefficiencies. To remain competitive, HFT firms must constantly invest in and upgrade their sophisticated infrastructure—both software and hardware—while staying on top of technological advancements. This makes HFT a highly complex sector, where companies are required to reinvest continuously in cutting-edge trading platforms. Like other high-tech industries, failure to invest properly, or making the wrong investments, can quickly lead to a firm falling behind its competitors.

Moreover, HFT is notoriously opaque, making it difficult for outsiders to assess a company’s competitiveness. Some reasons for this lack of transparency:

Proprietary Algorithms: HFT firms have developed highly sophisticated algorithms which they want to keep secret from their competitors to maintain their competitive edge..

Speed and Volume: Speed and volume of HFT makes it difficult for non-experts to grasp what is happening in real time.

Dark Pools: Many HFT firms conduct a significant portion of their trading in dark pools, private exchanges where trading activity is hidden from the public.

Constant Technological Evolution: HFT firms are constantly adopting new technologies to stay ahead.

Even regulators who can get more transparency find it hard to keep up with HFT firms.

In addition to the above reasons it is made even more opaque in that the key firms with market share such as Citadel are private firms. This means it is difficult to get an idea of overall industry profits and margins and so get an idea of how a firm is going relatively speaking.

Beware of ‘Clever’ Ideas Leading to the Trap of Confirmation Bias

Confirmation bias is the tendency to look for or interpret information that is consistent with existing beliefs and expectations.

When I first encountered the idea of investing in a HFT firm that would outperform during periods of market volatility and provide extra cash at ideal times, I was excited. This excitement led me to actively seek out information that supported the idea, while downplaying or outright ignoring information that raised red flags. I overlooked the complexities and opacity of the HFT industry simply because I was enamoured with the potential of investing in such a company.

Reflecting on how confirmation bias affected my decision-making, I’ve identified some strategies to help counter this in my investment process:

Structured Analysis: The structured analysis I’ve been developing on this blog is part of my effort to bring more discipline to my investment process. All of my initial investment theses follow a similar format, essentially acting as a checklist of key factors I consider important. This structure helps ensure that I cover critical areas and allows me to revisit mistakes—like this one—so I can refine my approach and avoid similar pitfalls in the future.

Evaluate Product Quality: What has changed my mind about Flow Traders was realising Flow Traders was losing market share.. The decline could have been due to underinvestment in their trading platforms, poor management decisions, or other factors. If I had focused on finding a way to monitor the quality of Flow Traders' trading systems—rather than just building a theory around market volatility—I might have avoided this investment.

Going forward, I plan to seek out more quantitative performance indicators, such as market share or comparisons with competitors, to better assess the quality of a company’s products or services. This is something I’ll need to think about for my existing investments.

Importance of a Margin of Safety

One aspect I believe worked in my favour with this investment was ensuring a solid margin of safety. When I published my article on Saturday, December 23rd, the next trading price for Flow Traders was €18.04 on Wednesday, December 27th. Today, the price sits at €18.65. At the time of my analysis, the stock was trading at 14 times earnings and 7 times free cash flow. Additionally, Flow Traders had about €584 million in trading capital, compared to a market cap of roughly €823 million—meaning around 71% of their market cap was backed by trading capital.

By buying with a good margin of safety, even though my thesis didn’t pan out as expected, I didn’t lose much.

Flow Traders Exit Strategy: Reflections and Next Moves

In hindsight, my investment in Flow Traders didn’t perform as I had initially hoped. The company’s declining market share, worsening financial results, and the complexity and opacity of the HFT industry have all contributed to my decision to exit this position. While the idea of owning a stock that would thrive during market volatility was compelling, I overlooked key risks and allowed confirmation bias to influence my analysis.

That said, one thing I did get right was ensuring a solid margin of safety when I entered the investment. Thanks to this, I haven’t lost much on the stock despite the underperformance. Because of this margin of safety, I’m not in a rush to sell my shares, but I do plan to exit the position over time. Moving forward, I’ll be more cautious about investing in complex industries and will continue refining my analysis to avoid similar mistakes in the future.